The grocery industry was rocked this week by the FTC’s unexpected decision to block the long-anticipated Kroger and Albertsons merger. For more than two years, the potential consolidation promised to reshape the competitive landscape, positioning the combined entity to rival industry giants and leverage economies of scale to improve pricing. With that option off the table, Kroger and Albertsons now face unique challenges and opportunities as they work to strengthen their individual market positions in a fiercely competitive environment.

At Prodege, we decided to dig into our Pulse consumer opinions about these two retailers, leveraging survey insights from over 200,000 verified shoppers collected from 2022 to 2024. Here’s what we learned about their positioning and how both retailers—and the broader grocery industry—can move forward.

Kroger vs. Albertsons: Shopper Sentiment Insights

Our data reveals key differences in how shoppers perceive Kroger and Albertsons, offering a snapshot of their current strengths and weaknesses:

- Shopper Loyalty: Kroger enjoys a stronger connection with its shoppers than Albertsons, as evidenced by a higher Net Promoter Score (NPS) of 51 versus 37 and top box preference ratings of 48% versus 37%.

- Pricing Perceptions: While neither retailer is seen as a low-price leader, Kroger outperforms Albertsons in several price-related attributes:

- Good prices: 35% (Kroger) vs. 26% (Albertsons)

- Good value: 37% (Kroger) vs. 28% (Albertsons)

- Lowest prices: 23% (Kroger) vs. 14% (Albertsons)

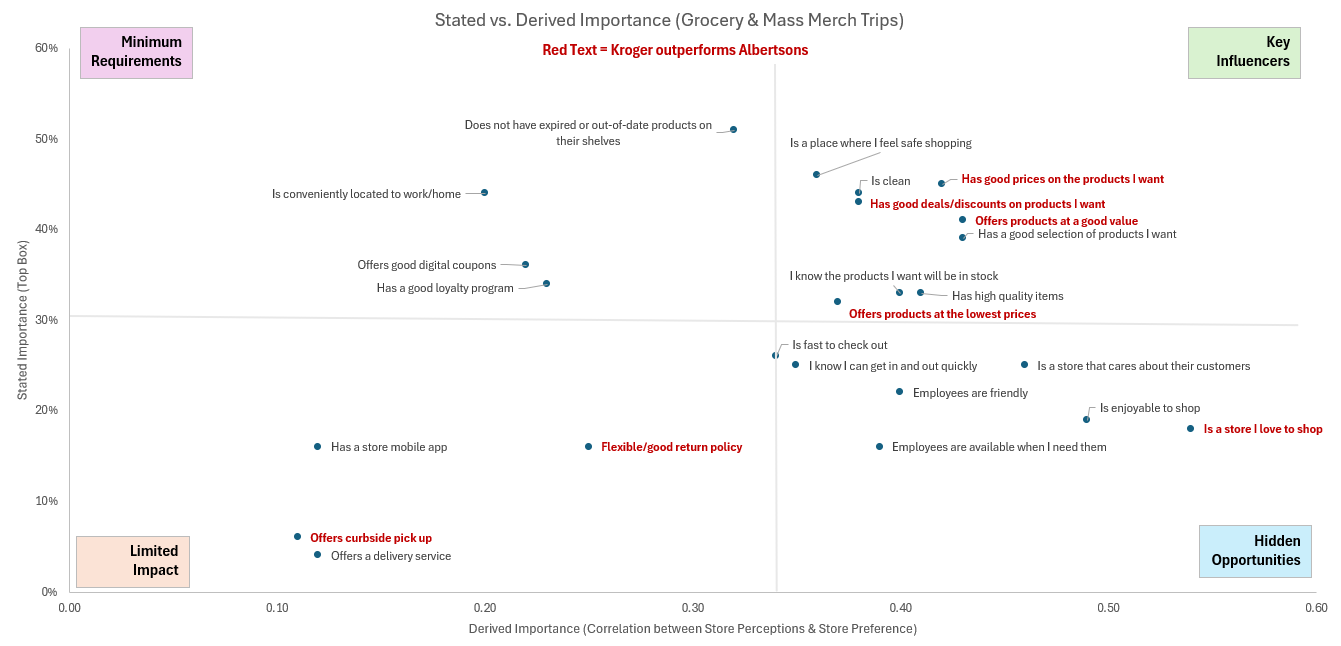

Key Takeaway: Price is the most critical factor driving store choice, yet neither Kroger nor Albertsons excels in this domain. Kroger, however, holds a relative advantage in shopper perceptions of value.

The Hidden Opportunities: Experiential Attributes

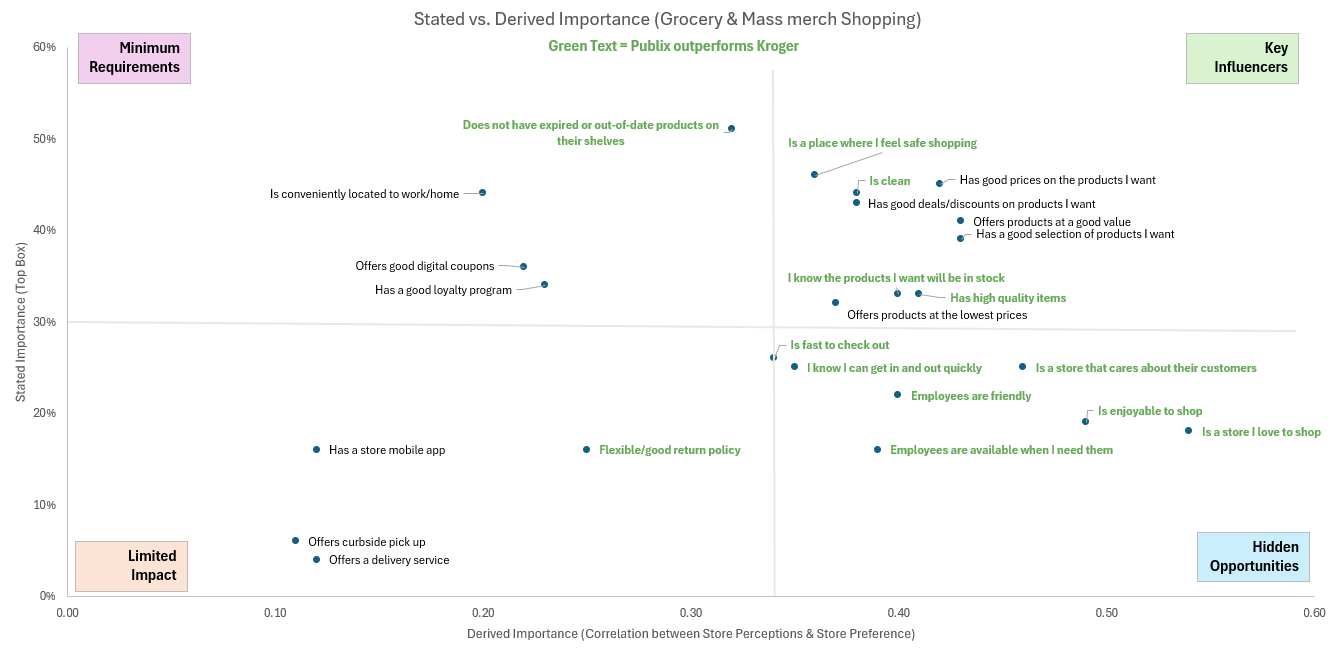

Beyond price, there are opportunities for both retailers to differentiate themselves through shopper experience. These are areas where Kroger has an edge but still falls short compared to high-performing regional competitors like Publix and Wegmans:

- Enjoyable to Shop: Shoppers find Kroger stores more enjoyable than Albertsons.

- Cares About Customers: Perceptions of customer care are stronger for Kroger.

- Employee Interactions: Kroger shoppers rate employees as more friendly and available than Albertsons shoppers.

Competitive Pressure: Regional operators such as Publix and Wegmans significantly outperform both Kroger and Albertsons at shopper experience. Publix, for instance, with plans to expand into Kroger’s backyard, Kentucky, with 12 new stores, poses a direct challenge to the Cincinnati-based chain’s market dominance.

Inflationary Pressures and Rising Competition

Both Kroger and Albertsons are navigating an increasingly challenging environment marked by:

- Inflationary Pressures: Rising costs of goods and operations are squeezing margins, forcing grocers to find efficiencies without alienating price-sensitive shoppers.

- Big Box Competition: Walmart, Target, and Costco continue to capture market share with their ability to offer low prices, one-stop shopping, and strong private label programs.

- Value-Focused Channels: Dollar stores and discount grocers are gaining traction with competitively priced offerings, appealing to budget-conscious consumers.

Strategic Challenge: For Kroger and Albertsons, competing on price alone is difficult against such giants. They must double down on differentiators like shopper experience, personalized promotions, and loyalty programs to protect their place in the market against expanding regional stores that deliver superior shopper experiences.

Post-Merger Fallout: What’s Next for Kroger and Albertsons?

Now that Kroger can no longer join forces with Albertsons to achieve stronger price positioning, both retailers must focus on other strategies to retain and grow their shopper base. Here’s what’s at stake:

- For Kroger:

- Compete with regional players like Publix by doubling down on shopper experience improvements.

- Leverage its stronger pricing perception and loyalty programs to build deeper connections with customers.

- Address inflationary pressures by optimizing private label offerings and operational efficiencies.

- For Albertsons:

- Address weaker shopper sentiment by focusing on experiential improvements, such as employee availability and customer care.

- Reevaluate pricing strategies to close the gap with competitors like Kroger.

- Strengthen partnerships with manufacturers to offer compelling promotions and exclusive deals.

The Broader Industry Implications

The FTC’s decision highlights growing scrutiny of industry consolidation, raising questions about how grocers can evolve in a fragmented marketplace. The competition from big box retailers and value-focused channels is intensifying, and traditional grocers must find innovative ways to remain competitive. Collaboration between retailers and manufacturers will be key to delivering value and creating exceptional shopping experiences.

Conclusion: The Path Forward

Kroger and Albertsons now face a pivotal moment. For Kroger, the challenge lies in maintaining shopper loyalty while competing with expanding regional operators like Publix and battling rising competition from big box stores. For Albertsons, the priority must be to address pricing and experiential weaknesses to stay relevant in an increasingly crowded and value-driven market.

As the grocery industry adapts to these shifting dynamics, one thing is clear: the race to win the hearts—and wallets—of shoppers is far from over. Retailers and manufacturers must work together to deliver both value and exceptional experiences in a rapidly evolving market.

About Prodege’s Pulse Syndicated Surveys

Pulse is a syndicated source of continuously collected consumer use and interests. Leveraging Prodege’s proprietary communities and our verified purchase behavior technology, we provide insights from American consumers about the products they buy, the retailers they visit, and other trending topics: Economic Attitudes, Media Engagement, Technology Opinions, Travel Planning, and CPG Path to Purchase. This database creates a wealth of information for retailers and brands alike. To learn more contact connect@prodege.com.

Written by Andrea Scheuerman, VP, Data Analytics at Prodege.

Bridget Tirella

Share This Article

Recent Press Releases

Prodege and McDougall Communications Forge Innovative Partnership to Advance Vision Correction ResearchEL SEGUNDO, Calif., Dec. 11, 2024 (GLOBE NEWSWIRE) -- Prodege Insights, a leading provider of consu [...]

Prodege’s Quality Audience Powers Market Research Platform PollfishAddition of 6,979 New Behavioral Targeting Criteria Improves Audience Quality EL SEGUNDO, Calif. [...]

Prodege to Present Ground-Breaking Conversational AI Insights with Procter & Gamble and Innovative Market Research with Panera Bread on Oct 8 at The Market Research Event (TMRE) in Orlando, FLAEL SEGUNDO, Calif., Oct. 03, 2024 (GLOBE NEWSWIRE) -- Prodege, a leading provider of consumer insig [...]